Atalaya is a small, copper miner, producing from a single mature mine in Spain. Its listed on AIM/TSE. Mkt cap is around 700m Euros. I was attracted by the dividends.

Operations

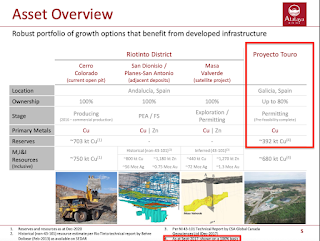

They have been producing from their Cerro Colorado pit in the RioTinto mine near Seville (south Spain) since 2016. From their 2022 production guidance (15.5Mt/year) and Proven Reserves on their website (128Mt @ 0.41% cutoff), the mine has 8 years life remaining. Their June 2021 reserve estimate gives proven reserves of 139Mt @ 0.38% Cu, estimating a 12 year lifespan (ie: 11 years from now). So this mine's lifespan is somewhere between 8 and 11 years.

They have new mine (Touro) in the north of Spain undergoing permitting. This has half the reserves and roughly half the potential production of Cerro Colorado:

And like any mining company, they have a number exploration projects ongoing. Most are surrounding RioTinto:

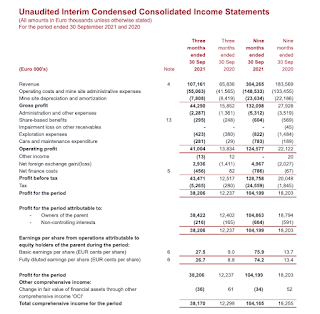

Finances

Risks

They are producing from a single mine. Anything that goes wrong there affects their entire production.

Cerro Colorado only has an 8-11 year lifespan. Production should start soon at Touro, but this is only half the size. They need more projects to work out, just to replace Cerro Colorado.

Not much Geopolitical risk. I like to own copper production away from Chile and Argentina, who are raising resource taxes.

I think Spain's gonna have a currency crisis and leave the EU, but that doesn't affect mining. And I think Spain is not as safe a jurisdiction as Canada or Australia, but its better than Latin America or Indonesia. With mining you can't be choosy.

Misc

Spain has a 19% withholding tax. Should be 5% for Singapore residents (p7), but I'll need to see what Interactive Brokers charges.

I got this idea from an 2021 interview (paid link) on CruxInvestor. He starts talking about Atalaya's projects at 22:00. Dividends and acquisitions/mergers at 27:00. Expansion at 39:40.

Conclusion

No comments:

Post a Comment