Worlds largest luxury goods seller. 2010 revenue/profit breakdown:

- Fashion & leather goods (38%/62%)

- Wine & Spirits (16%/22%)

- Perfume + cosmetics (15%/8%)

- retailing (27%/5%)

- watches + jewelry (4%/3%)

First we look at the first 2 segments separately.

Leather and FashionI never imagined that I would ever, in my entire life, see a line of people

queuing to shop for thousand dollar handbags.

It is difficult to convey how luxury goods are a part of everyday life here. The car you drive, the watch or clothes you wear, do really mean something. Women can instinctively identify a myriad of branded handbags, jewelery and watches at a glance.

The book "

The Cult of the Luxury Brand", believes that Asian countries follow a model in their adoption of Luxury goods; the final stage is where Japan is now, where it is a 'way of life'. They write about the ubiquitous LV in Japan: "It is well past the stage of a trend, it has become an enduring requirement - like sushi or green tea - essential to the Japanese way of life...the company has taken the trend to conform to its logical end: To be Japanese means to have a Louis Vuitton bag. The brown bag with the original monogram pattern and pale leather trimmings has come to define the Japanese national identity."

In short, luxury goods are not a luxury. They are a part of everyday life. From junior office ladies to tai-tais, many people here must have them to function in society. This bodes well for the continuing consumption of luxury goods, which can be supercharged by an emerging China and India.

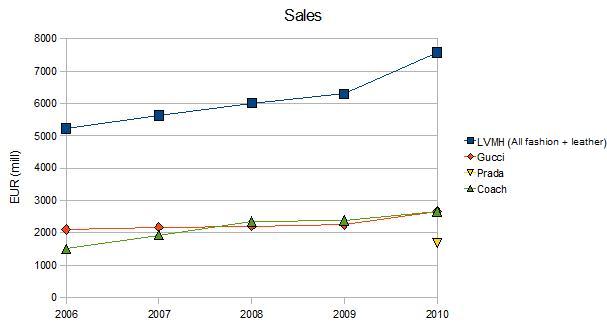

Comparing sales and profit margins of other brands with LVMH is hard, because LVMH does not break down sales for the many brands they own (LV, Fendi, Donna Karan, Loewe, Marc Jacobs, Celine, Kenzo, Giovenchy, Thomas Pink, Pucci, Belutti, Rossimoda). The chart below show show the total amounts for 'fashion and leather' for LVMH, compared with individual brands for other companies (so not really an apples-to-apples comparison):

From the above, their flagship LV brand, has,

at most, twice the sales of the nearest competitor.

[For Coach, converted to Euros at a rate of 1 USD = 0.7394 Eur]

LVMH's margins are among the highest in the industry, only occasionally surpassed only by coach. The LV brand itself would probably have even higher margins, as they are lumping in all brands together.

LVMH's 'leather and fashion' revenue did not fall during the 2008 crisis. It may have been due to China, LV did not break down the figures.

Wine & Spirits2010 revenue and profits are split evenly between "Wine/Champagne" and Spirits.

The

champagne market is highly fragmented, with many producers.

This article (free

here) puts MH at an 18% global market share. It also discusses how MH is trying to tie up supplies in the (govt mandated) champagne growing regions. I would put MH as the largest player in a fragmented field, but with no real dominance or pricing power.

The champagne/wine market is

highly cyclical, as with any commodity that has a fluctuating price and takes time to grow. e.g.: c

hampagne grape glut in 2009,

wine grapes in 2003.

For spirits:

- MH trails the largest playes in the spirits market (2010 revenue: 3.3 bn Euros). The largest player is Diaego (revenue: 15 bn Euro) and Pernod-Ricard (June 09 revenue: 7 bn Euros).

- MH's products do not appear in the top lists for spirits.

- HM has a 44% share of the cognac market. Cognac went out of fashion in the early 90's, but is now revived due to rappers and China.

HM is not a leader in this market. The Champagne market is highly cyclical. And the spirits market is subject to changing fads and fashions.

Business Model and RisksFor the company as a whole, about 10% of their revenue is spent on advertising.

In the luxury goods business, the main aim is to develop a 'buzz'. Usually done by having celebrities and A-list people wear your products, appear at your parties, etc. This creates a fashion, which people talk about and want to imitate.

This 'buzz' is the heart of the luxury goods business - it feeds it and is fed by it. I'm not sure exactly what creates it, but its more than throwing millions of dollars at advertising.

LVMH's income statement is quite sketchy: cannot tell how much of their costs are variable and how much are fixed. The financial statements are short: LV does not even break up their sales/margins by brand; contrast to Coach for example, which provides same store sales.

The chairman,

Bernard Arnault, owns 47% of the company and has direct control. Two of his five children currently work there: Antoine Arnault has a

management role and is on the board of directors,

Delphine Arnault is a director, and nephew Harry Seaman may be involved as well.

LVMH owns many unrelated businesses. Ranging from a stake in Hermes (designer bags costing 50K), to cosmetics retailer Sephora (similar to 'Watsons', but for cosmetics), to

Charles & Keith ($30-$40 women's shoes). Does not seem to have any focus. Combined with their sketchy financial information, makes it hard to track.

To conclude:

- LVMH's main business is Fashion and Leather goods. The others are just sidelines or distractions. And are in more competitive markets, so unlikely to make the same margins as leather goods.

- This is the only area they have have a competitive advantage in. The LV brand probably sells twice as much as its closest rival, and has the industry's highest operating margins.

- This market has the potential to boom, thanks to China/India.

I'm not sure if I'd be comfortable buying this stock.

REITS

REITS

{kind=link}