Half my portfolio are companies that rely heavily on debt. REITs or infrastructure. Need to quantify how much rising rates could affect them.

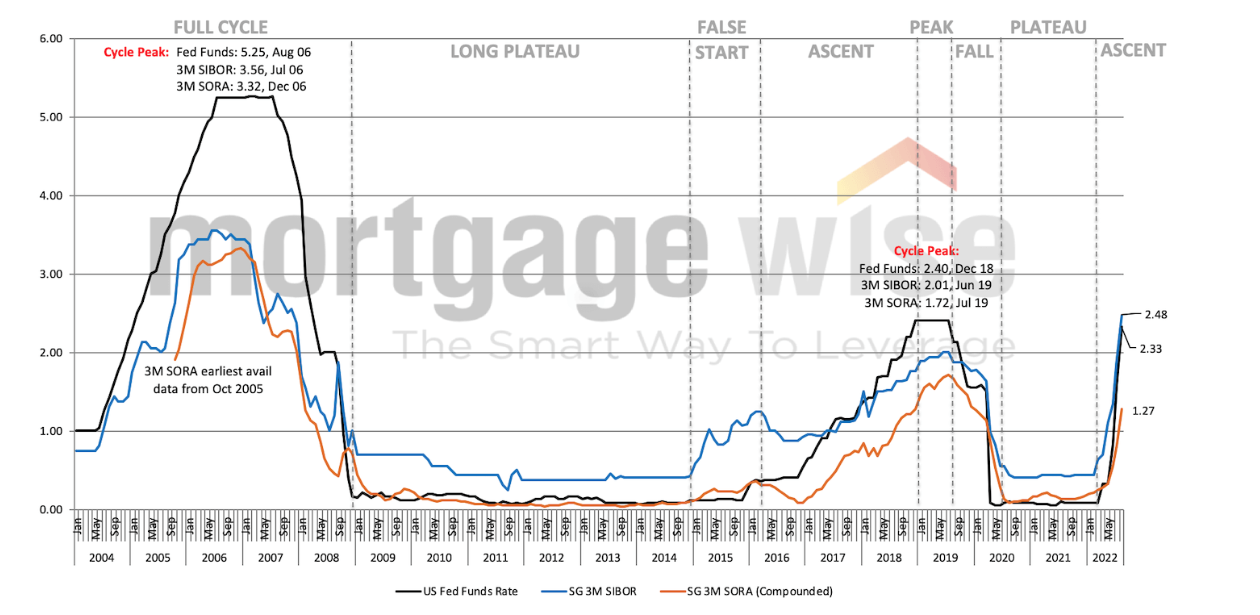

Powell has said he will raise rates as high as necessary to curb inflation. I''ll assume he gets to 5% in 2023, same as in 2006:

I expect a fed funds rate of 5% in 2023 to cause a recession. Then lower rates in 2024/2025, maybe 2-4%, which cause inflation. Then higher rates of 5-6% after that. Don't think we'll get back to zero.

I'm testing 2 scenarios:

- Scenario 1: By end 2023, we get a Fed Funds rate at 5% and SOR at 3.5%. BBB rated companies pay 7.5% for USD debt, and 5% for SGD debt.

- Scenario 2: Extend the same rates to the end of 2027.

Williams Companies

14% of my portfolio. Their debt is all fixed rate and widely spread out till 2051:

Source: WMB 2021 AR (p110).

I assume refinancing at 7.5% for notes and 9% for debentures:

- For scenario 1: 2021 CFO would have dropped by 3.3%.

- For scenario 2: 2021 CFO would have dropped by 10%

Frasers Centerpoint Trust

11% of my portfolio. Most of their borrowings are from bank loans, with a small amount from MTNs:

I could not find whether these bank loans were fixed or variable, or their interest rates. Despite scrolling through years of SGX filings. Note 16 in their Annual Report has 3 pages of numbers, but I could not find the tenor or terms of the majority of their borrowings.

Note 14 says that 430m of their debt was hedged using swaps. I could not see when the swaps expire. A Phillips Securities report suggests "the tenor of the hedge is usually matched with the debt maturity profile."

So this business that is based on debt is vague about the details of its debt. There is a reason why US stocks trade at a premium.

Effects of rising rates?

- Scenario 1: Interest payments increase by 5.5m to 9m. 2021 Distributable income would have fallen by between 2.1% to 3.7%.

- Scenario 2: 2021's Distributable income would have fallen by 20%.

Kinder Morgan

10% of my portfolio. Like Williams Companies, KMI's debt is almost all fixed (pp99-100). And its also rated Baa2 (equivalent to BBB).

I assume refinancing at 7.5% for notes:

- For scenario 1: 2021 CFO would have dropped by 3.5%.

- For scenario 2: 2021 CFO would have dropped by 6.7%

Frasers Logistics and Commercial Trust

10% of my portfolio. Rated BBB+.

March 2022's debt is SGD 2.8b. Only 170m is due in 2023:

Source: 1HFY22 Results Presentation

I do not know the interest payment on that 170m, or if it is fixed or floating:

Source: Note 18 2021 AR

The percentages of loans in different currencies are:

They also use interest rate swaps (Note 14A 2021 AR). We don't know how much the debt the swaps cover, because they give nominal amount (value on balance sheet) instead of notional amount (the debt covered). The only useful information is that the majority of these swaps expire in 2-5 years (Sept 2023 to Sept 2026), and none extend beyond that.

Not much to go on. Best guesses:

- Scenario 1: Increased interest payments on the 170m for debt-due-2023. By around 4-8m. 2021's Distributable Income (p200) would have dropped by 1.5 to 2.9%.

- Scenario 2: All of their interest rate swaps have expired. Only 8% of the debt extends after 2026, but since I don't know how much, I'll just assume its all refinanced. Assume similar currency breakdown but remove the small currencies: 46% debt in SGD (at 5% interest), 18% AUD (at 5% interest) and 36% Euro (at 4% interest). Interest payments increase by SGD 87m. 2021's Distributable Income would have dropped by 32%.

Lend Lease Commercial Trust

7% of my Portfolio.

They provided good info in their previous AR, but debt has since doubled with the Jem acquisition. Wait for the next AR, probably October.

Fibra Macquarie

5% of my Portfolio. All borrowings are in USD (along with most of their revenue):

Source: Note 11: 2021 Results

Increasing rates lead to:

- Scenario 1: CFO drops 5.5%, AFFO drops 6%

- Scenario 2: CFO drops 19.5%, AFFO drops 19%

For this company, I would be concerned with the MXN/USD exchange rate. Even though their revenue and debts are in USD, it may be a strain for their customers to pay if USD shoots up too much against MXN. But the chart looks OK: peak to trough over the past year its only has a 9% drop, overall it looks flattish:

Ascendas India Trust

3.5% of my Portfolio.

As of June 2022 (p20):

- 62% of their debt is in INR, 38% in SGD.

- 79% of their debt is hedged (slide 13). Most of it is hedged by swaps. I could not see when the swaps expire (p196)

- 17% of their debt is due in 2023 (slide 13). Most of it INR.

I don't know anything about Indian interest rates, except that their central bank hiked to 5.9% yesterday. Assume they reach 6.5% next year, and the swaps for 2023's debt expire with it. Assume AIT's INR new borrowing costs are 8.5%. Assume all swaps expire by 2027.

We get:

- Scenario 1: 1H2022 Income available for distribution drops 3.7%.

- Scenario 2: 1H2022 Income available for distribution drops 17%.

Conclusion

My SGX REITs:

- show a 17 to 32% define in distributions of the Fed Funds rate gets to 5% for 5 years.

- while I can't calculate the effects of rising rates for 1 year as I do not know details of their loans and hedging.

- and (except for Ascendas India Trust) they also pay out 100% of their distributable income, meaning they can only reduce their debt by issuing shares.

WMB and KMI are less affected due to their decades-long-term fixed-rate debt.

No comments:

Post a Comment