Heres the details:

- What are AAV's realised prices compared to the benchmark? The company gives their realised price and the AECO price (in CAD/mcf) in their quarterly results:

Showing just the discount:

Around 0-30 cents. The discount to the Benchmark is pretty small, unlike in the Marcellus. Sometime even negative! Lets take 20c. Though theres a risk that the discount may widen if too many companies start producing in the low cost Montney area.

- Look at the Natural gas futures prices.

Source - gasalberta.com (as of 6-Jul-2016). Great source for simple AECO and NYMEX prices.

AECO price is in CAD/GJ, which is approximates very roughly to CAD/mcf (100 GJ = 94 mcf). So multiply by (100/94) to get mcf price.

- Look at AAV's projected production. In 2017 they project 245 thousand mcf/day, which is an 1.83 times their 2015Q1 daily production. From the above futures chart, CAD 3.07 (per GJ) is about CAD 3.26 per mcf.

- Based on their 1Q2015 profits, project what their profits would be at different gas prices in 2017. I am using a discount of 20c. Usually I would go through the income statement and guess which of their costs are fixed (e.g.: General & Admin) and which are depend on production volumes (e.g.: operation expense, DD&A). But for AAV it didn't make much difference (mostly variable costs), so I just multiplied their profits proportional to the expected production increase. I get:

Highest I can get is CAD 3.90 at the 2019 price. At USD 6 plus (~ CAD 7.80) , the stock is overvalued. My ballpark figures can't even get close.

[Edit: 4th Aug:

Producing gas cheaply is not enough, you also have to deliver it to customers. Canada has a small population of 35m. Monty, in West Canada, has historically exported gas to East Canada and the NorthEast US. Both are under threat by prolific US production there, especially in the Marcellus. I think that Canada's Montney gas production will rely on LNG exports to Asia.

Thats a big uncertainty. I don't know enough about the industry to buy gas producers in a new emerging area.]

[Edit: 4th Aug:

Producing gas cheaply is not enough, you also have to deliver it to customers. Canada has a small population of 35m. Monty, in West Canada, has historically exported gas to East Canada and the NorthEast US. Both are under threat by prolific US production there, especially in the Marcellus. I think that Canada's Montney gas production will rely on LNG exports to Asia.

Thats a big uncertainty. I don't know enough about the industry to buy gas producers in a new emerging area.]

Price/EBIDTA or Price/Cashflow

Most analysts I've seen use price/EBIDTA or Price to Cashflow (not sure which cashflow...) to value Oil and Gas E&P companies. You get much lower multiples, because these denominators exclude Depletion, Depreciation and Amortisation (DD&A), which is the largest component of costs for most Oil and Gas companies. For AAV's 1Q 2015 results for example, DD&A was around 2/3rd of their expenses:

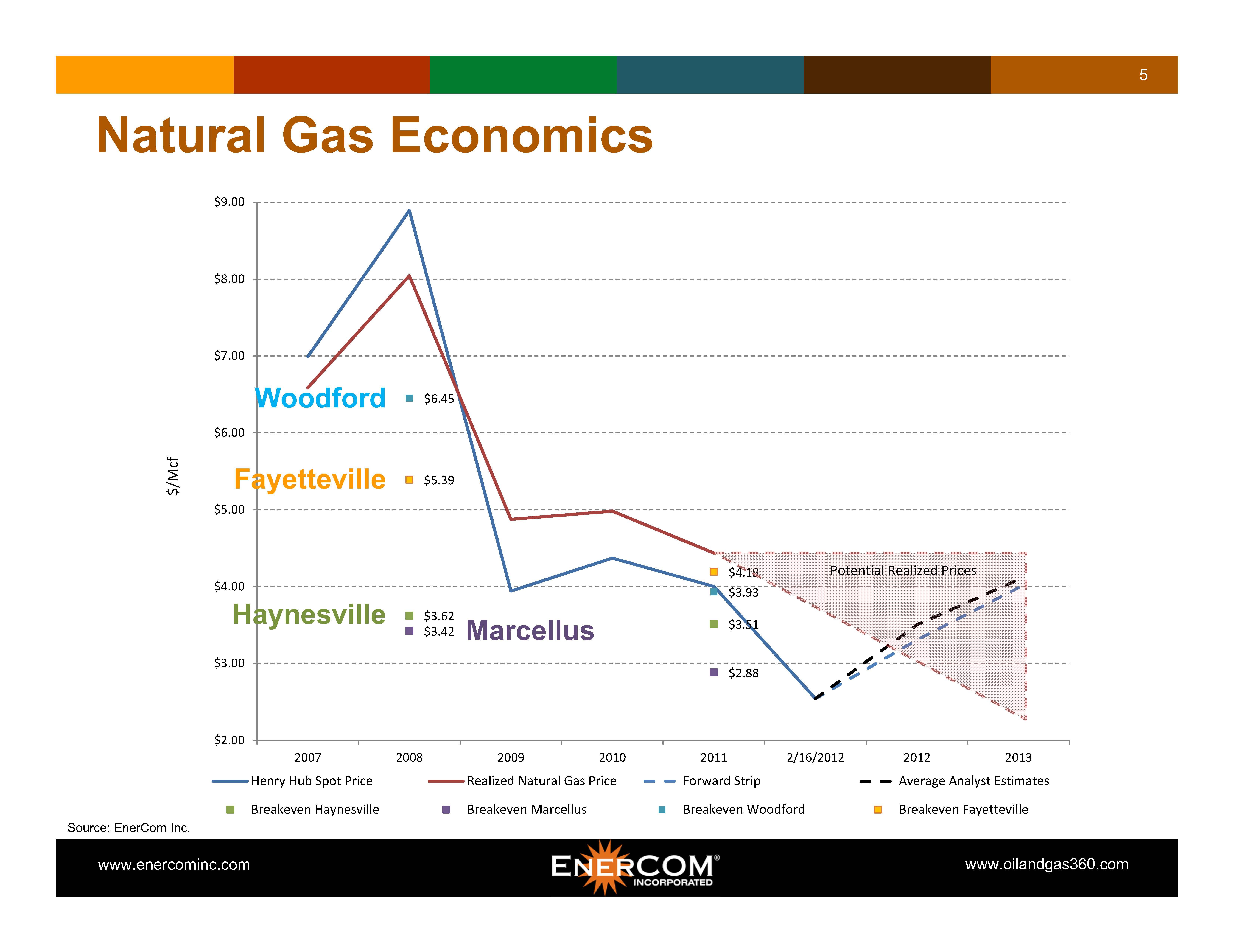

It doesn't make sense to exclude DD&A from the valuation, and also exclude the Cash Flows for Investment needed to drill new wells to make up for the depletion. Especially when shale wells deplete so rapidly. For example, AAV's 2015 June investor presentation (p5) shows hyperbolic decline curves for wells drilled in different years:

I cant see why analysts use price EBIDTA or price/cashflow metrics. This applies to all oil and gas E&Ps, not just AAV. I just don't get it.

{kind=link}