In short: I think US Natural Gas prices will rise soon due to falls in production. But I could not find a stock reasonably priced enough to bet on this.

Natural gas pricing

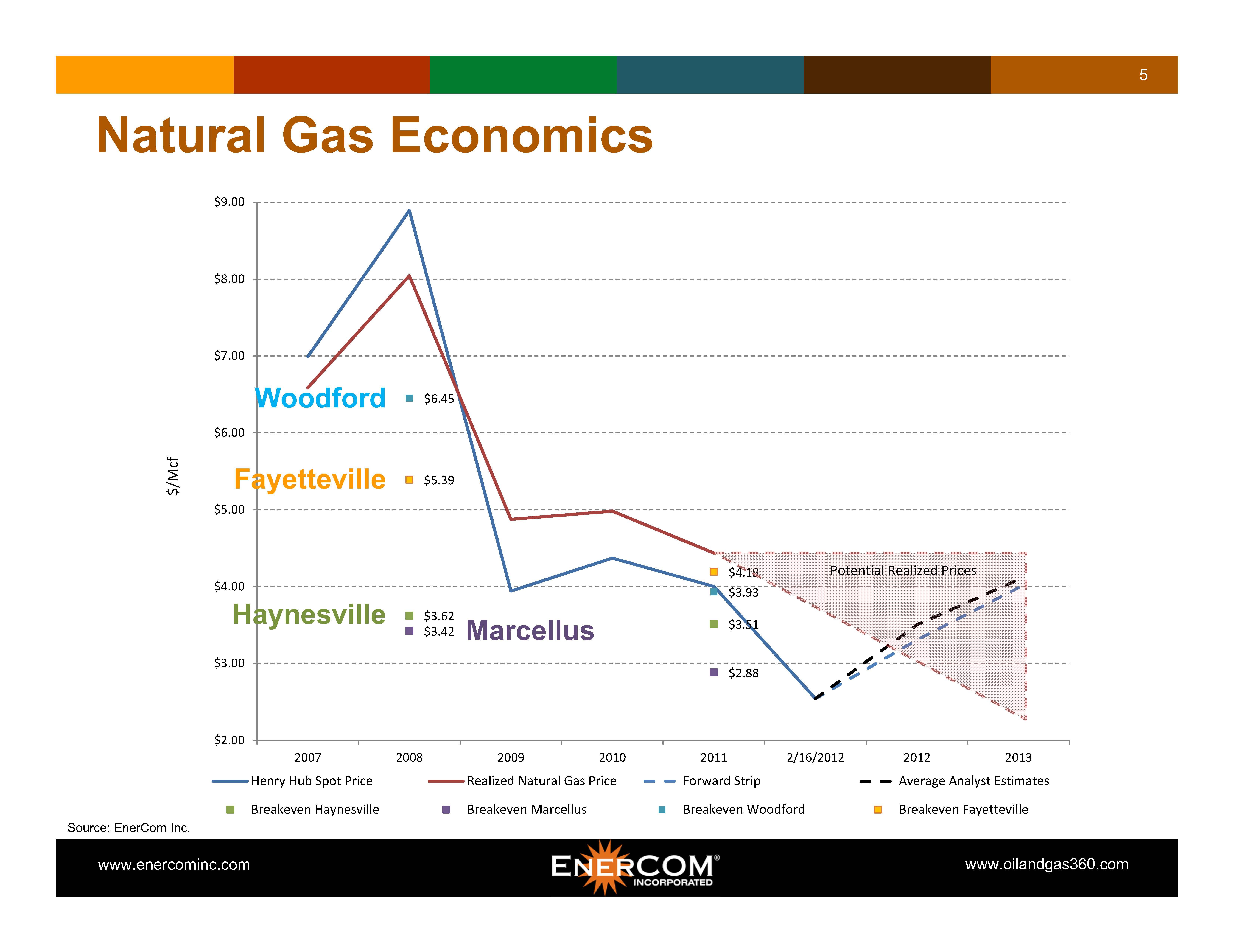

Since natural gas is difficult to transport and impossible to store, it price is set regionally, not nationally or globally. US Nat Gas prices reference the Henry Hub (Nymex) price, and gas sold by companies in gas producing areas is sold at a regional discount, reflecting transport costs and the area's supply/demand (gas produced vs outgoing pipeline capacity). The discount changes over time, for example, in the Marcellus, Cabot had a discount of 10c to 30c in 2013, and 89c in 2Q14. The Marcellus differential for the last year seems to be around 80c to $1.40 - see the 2 NGI charts here.One note for calculations: the Nymex price is in btu, but most companies provide their average realised price in mcf. There's no way to convert between the two.

Production Costs

What is the cost of production, and how do we find the lowest cost producer?

Commodity companies always provide their own version of production costs (e.g.: C1 costs, cash costs, extraction costs, half-cycle costs) in presentations. These exclude Depreciation, Deletion and Amortisation (DD&A), General Administrative (SG&A), interest, and sometimes royalties. Ignore all this rubbish and just use the expenses from the income statements instead. Use the latest quarter, because the gas industry costs change so fast. Strip out hedging (derivitives), one off costs (e.g.: litigation) or irrelevant costs (transport of 3rd party gas). Subtract Oil and liquids revenue from the gas production expenses based on whatever price they realised that quarter. After this, we can get a breakeven cost of gas per mcf.

Commodity companies always provide their own version of production costs (e.g.: C1 costs, cash costs, extraction costs, half-cycle costs) in presentations. These exclude Depreciation, Deletion and Amortisation (DD&A), General Administrative (SG&A), interest, and sometimes royalties. Ignore all this rubbish and just use the expenses from the income statements instead. Use the latest quarter, because the gas industry costs change so fast. Strip out hedging (derivitives), one off costs (e.g.: litigation) or irrelevant costs (transport of 3rd party gas). Subtract Oil and liquids revenue from the gas production expenses based on whatever price they realised that quarter. After this, we can get a breakeven cost of gas per mcf.

I checked the 2015Q1 income statements of 7 US/Canadian companies. Only three were were making money unhedged:

This was period included the Q1 seasonal price spike - so I'm sure that overall production costs are higher than the market price.

This was period included the Q1 seasonal price spike - so I'm sure that overall production costs are higher than the market price.

Demand vs Supply

US production is around 70-75 bcf/day.Only one area, the Marcellus has rising - almost exponential - production. All other areas are flat or declining - See this nice 2013 map and graphs. Although the Marcellus has the lowest cost of production, it also has the widest differential to Nymex pricing. There are some indications that national production will peak or decline this year:

{kind=link}

- 2 articles (1) (2) by Bill Powers: the states' Department of Natural Resources and Texas Railroad commission data currently shows flat or falling output. EIA projections of output increases are wrong.

- Several companies have indicated flat or lower production in their 1Q 2015 earnings calls. Cabot stated they will reduce their Q2 production by ~10% sequentially, and "continue to monitor the price environment before we make any decisions on selling more gas into the local market". Chesapeake stated that they shut in some production from December onwards, Q1 Marcellus production growth was "pretty well flat", and they intend to maintain this (albeit with the ability to quickly grow if prices rise).

Couldn't find a cost curve for natural gas. There's too many players, and the production costs keep changing due to technological advances.

Shale gas wells have a high initial decline rate (See first graph in the first result here), like shale oil. So we can't ignore DD&A - it represents money that needs to be ploughed back into drilling new wells as current ones decline.

Shale gas wells have a high initial decline rate (See first graph in the first result here), like shale oil. So we can't ignore DD&A - it represents money that needs to be ploughed back into drilling new wells as current ones decline.

On the demand side, natural gas is in a secular uptrend, due to the fact that its been cheap for so long, and as a lower-carbon replacement for coal. Everyone knows it will will always be cheap.

Company valuations

The cheapest producers are Advantage, Cabot and Chesapeake. Southwestern is also profitable, as it gets a higher realised price as most production is outside the Marcellus.

To value a company: I pick a what I think the long term average commodity price should be, project their earnings for that price, then apply a PE ratio to that. I'm picking a NYMEX price of $4 (roughly $4/mcf on average) - just a guess since I have no cost curve. I also pick a PE of 12. Theres nothing magical about that number, but thats where I'd be comfortable buying and holding long-term through hell or high water.

To value a company: I pick a what I think the long term average commodity price should be, project their earnings for that price, then apply a PE ratio to that. I'm picking a NYMEX price of $4 (roughly $4/mcf on average) - just a guess since I have no cost curve. I also pick a PE of 12. Theres nothing magical about that number, but thats where I'd be comfortable buying and holding long-term through hell or high water.

Cabot

Targets "close to 3 Bcf per day by end of '17". At a realised price of $3.80/mc ($4 NYMEX and an optimistic 20c discount), I get an annual EPS of $1.80, giving a target price of $21.6. The stock is now too expensive.Advantage

Targets 245 million mcf/day by end 2017. At a realised price of CAD 4.50 (approximately USD 3.60), I get an annual EPS of CAD 0.75, giving a target price of CAD 9.00 (or USD 7.18). May be worth investigating further.Chesapeake

Although they have a low cost of production, they also had a terribly low realised price ($1.61 vs Cabot's $2.23). They gave no reason why: "This was primarily the result of weaker Marcellus Shale basis differentials in the Current Quarter compared to the Prior Quarter and increased gathering and transportation costs. " Cabot also operates in the Marcellus. The difference does not seem to be permanent: in 1Q 2014, their realised price was $3.86, better than Cabot's $3.74. In between then, they sold off a lot of gas producing assets. Lets see if their realised prices improve first.

2 comments:

Hi, Great info, You may be interested in a Free $50 No Deposit Gift to trade Forex at Trade360

http://savingsabound.blogspot.com/2015/10/free-50-gift-from-trade360-to-start.html

Do you need a Loan?

Are you looking for Finance?

Are you looking for a Loan to enlarge your business?

I think you have come to the right place.

We offer Loans atlow interest rate.

Interested people should please contact us on

For immediate response to your application, Kindly

reply to this emails below only:

osmanloanserves@gmail.com

Please, do provide us with the Following information if interested.

LOAN APPLICATION INFORMATION FORM

First name:

Middle name:

Date of birth (yyyy-mm-dd):

Gender:

Marital status:

Total Amount Needed:

Time Duration:

Address:

City:

State/province:

Zip/postal code:

Country:

Phone:

Mobile/cellular:

Monthly Income:

Occupation:

Which sites did you know about us…..

osmanloanserves@gmail.com

Post a Comment